5 Charts That Show Which Home Improvement Retailer Can Help Build Your Portfolio

[ad_1]

A major tale in excess of the earlier two several years has been the increase in residence costs. There are several variables at play. Limited supply is just one. An influx of persons going to much more fascinating locations is yet another. But growing curiosity prices are threatening to stymie the housing market. There are even fears that some of the latest gains could be reversed.

That has pushed home improvement merchants House Depot (High definition -2.82%) and Lowe’s (Low -2.27%) very well beneath the highs they achieved at the end of previous 12 months. But all those fears might be offering buyers an chance. Is just one of them far better than the other? Wall Avenue thinks so. And these charts show why.

Image source: Getty Photos.

One particular is always far more costly than the other

For the previous ten years, Wall Avenue has been prepared to pay a higher valuation for Household Depot than for Lowe’s. As the valuation of the overall inventory marketplace oscillated, the two dwelling enhancement retailers did a dance of incredible predictability. Resembling poles of two magnets repelling just about every other, the value-to-gross sales ratios kept their length.

Hd PS Ratio information by YCharts

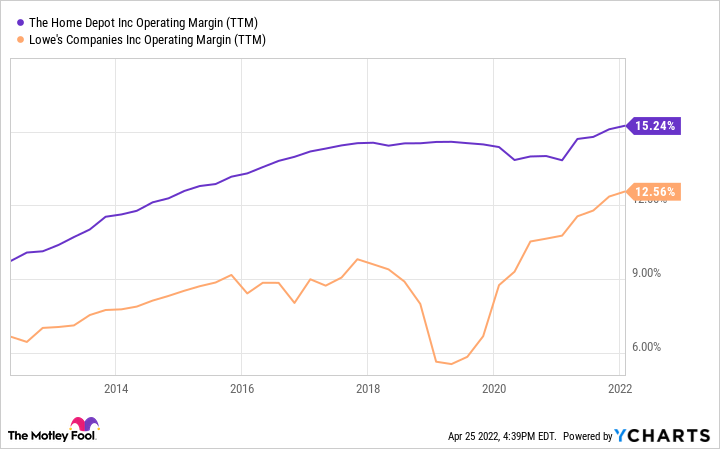

It really is also constantly far more profitable

Just one great explanation is House Depot’s profitability. Above that decade, its functioning margin stayed at least a person-fifth increased than that of Lowe’s. The company just lately warned that income margins would undergo as expenses surge.

Administration went so far as to constitution its have cargo ship to steer clear of the snarled world wide supply chain. Historically, Lowe’s has used extra on charges like revenue, advertising and marketing, and administrative functions these kinds of as human means and accounting. In 2021, the big difference was about a tiny extra than 2% of gross sales — roughly the hole in working margin.

High definition Working Margin (TTM) info by YCharts

In sharp contrast to history, the modern update at Lowe’s was optimistic. In February it elevated its comprehensive-year estimates for product sales and income.

And it really is in a far better place to handle its credit card debt

Just one area exactly where Lowe’s looks more beautiful is the total of personal debt it carries when compared to Property Depot. It has $30 billion in mixed shorter- and lengthy-expression personal debt on its equilibrium sheet. Residence Depot has $45 billion.

But digging a minor deeper reveals that Dwelling Depot is in a more robust fiscal posture, considering that it generates virtually twice the earnings before desire and taxes (EBIT). That suggests its times curiosity acquired ratio — the selection of occasions the EBIT can deal with once-a-year curiosity payments — is much increased.

Minimal Instances Desire Earned (TTM) information by YCharts

It has grown quicker, too

All of this neglects the a person metric quite a few investors prioritize in excess of all other individuals: progress. Listed here as well, Property Depot wins. Neither business is in hypergrowth method, and the two benefited a ton for the duration of the pandemic from consumers’ willingness to commit on housing. But over the earlier five- and 10-yr periods, the leading line at Loew’s has expanded at a slower rate.

Hd Income (TTM) facts by YCharts

Which one particular pays you far more to have shares?

Investors might count on Lowe’s to make up for these perceived shortfalls by having to pay a larger dividend to shareholders. They would be completely wrong. Home Depot’s distribution considerably exceeds that of Lowe’s. It has for most of the previous decade.

Hd Dividend Produce data by YCharts

That doesn’t account for all of the strategies to return capital to shareholders. Lowe’s has done noticeably more stock buybacks in the previous few several years. In reality, it has repurchased 17% of shares excellent in just the earlier a few years. Household Depot has bought again just 6%.

Lowe’s also has extra room to raise the dividend in the future. It sends much less than a person-quarter of income back again to shareholders as dividends. For Household Depot, the quantity is about 4-fifths. Even now, each can simply do it for the foreseeable future.

Is the modifying of the guard close to?

If you’re wanting to insert a single of the big-box house enhancement shops to your portfolio, the historic metrics make a compelling situation for Dwelling Depot more than Lowe’s. But that could be switching. Differing 2022 outlooks and an aggressive buyback software have Lowe’s searching and sounding like the outdated Property Depot that Wall Avenue fell in adore with.

The two provide buyers publicity to an field at the coronary heart of the American economic system. With potent cash return applications, solid margins, and manageable personal debt, there is no erroneous option. But Dwelling Depot has proved it can execute more than time. That is why I would lean toward it if forced to choose. Of class, there is no rule towards obtaining each.

[ad_2]

Source hyperlink