Performance Food Stock: A Somewhat Stable Business In Unstable Times (NYSE:PFGC)

[ad_1]

goc/E+ via Getty Images

Investment thesis

With the growth prospects and stability of Performance Food (NYSE: NYSE:PFGC) in mind, a forward P/E ratio of 15.58 is very reasonable, and that’s why I believe it’s a buy.

Table of contents

-

Introducing Performance Food

-

Market Opportunity

-

Competitive analysis

-

Growth analysis

-

Margin analysis

-

Valuation and Conclusion

Introducing Performance Food

The Performance Food Group Company markets and distributes food and food-related goods. Foodservice, Vistar, and Convenience are the company’s three segments.

The Foodservice segment sells to independent and multi-unit chain restaurants, as well as schools, healthcare facilities, business and industrial locations, and retail establishments.

Vistar specializes in the distribution of candy, snacks, beverages, and other items through vending, office coffee service, theater, retail, hospitality, and other channels.

Convenience segment: Candy, snacks, beverages, cigarettes, other tobacco goods, food and foodservice products, and other things are distributed to convenience stores.

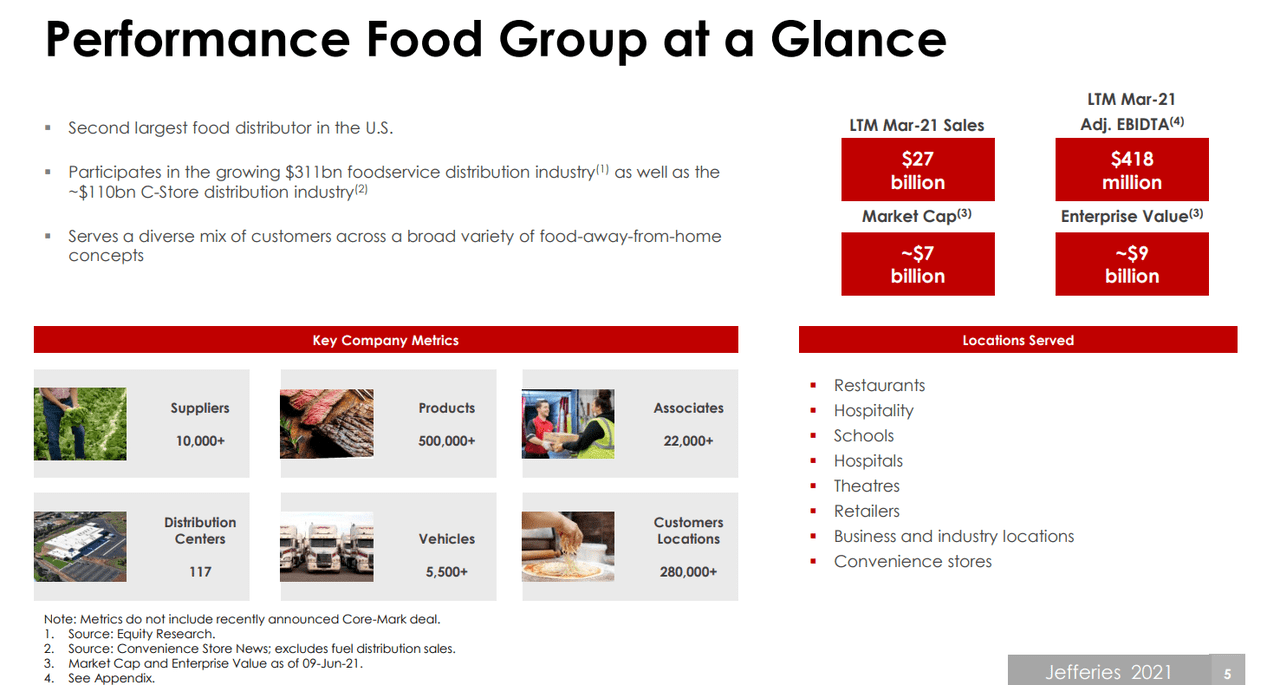

Performance Food Group at a Glance (Jefferies Virtual Consumer Conference June 2021)

Market outlook

Both the Foodservice and Foodservice Distribution industries are matured markets. For this specific reason, I expect that the growth rate of the industry is equal to roughly the economic growth rate, which is around 3 to 4 percent.

Also according to a Mordor Intelligence report, The US foodservice industry is expected to grow at a CAGR of 3.7 percent (2022 to 2027).

Competitive analysis

Performance Food is part of the foodservice market. In this article, I selected a peer called Sysco (NYSE: SYY) to benchmark Performance Food’s performance. Sysco Corporation also markets and distributes food and related items primarily to the foodservice or food-away-from-home industry.

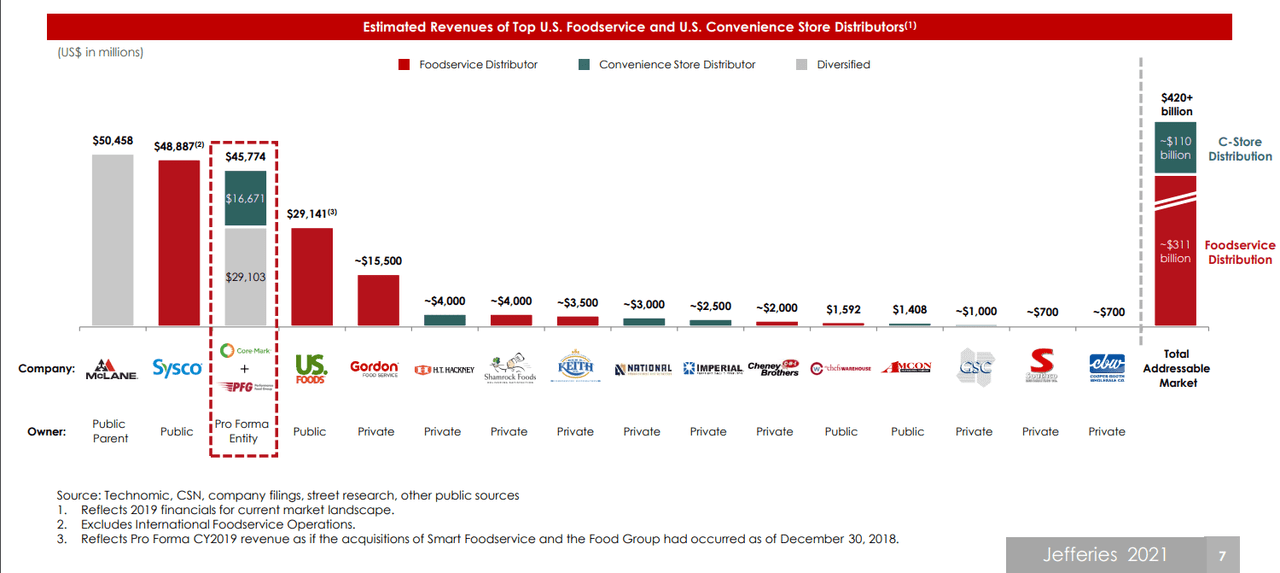

Performance Food is currently one of the largest foodservice distributors in the US:

Competitors (Jefferies Virtual Consumer Conference June 2021)

According to the annual statement, this allows for a competitive edge over regional and local broad line distributors due to purchasing and procurement economies of scale, which enable them to offer a wide range of products (including its proprietary Performance Brands) to its clients at competitive pricing.

However, there are still 2 companies with a bigger national footprint. Furthermore, Performance Group often does not have exclusive service agreements with its customers and its customers may switch to other distributors if those distributors can offer lower prices, differentiated products, or customer service that is perceived to be superior.

Overall, I’d say that the competitive position of Performance Group is alright.

Growth analysis

As revenue in the business segment will continue recovering from the Covid pandemic, I expect that the short-term growth rate will be high. Furthermore, depending on what inflation will be doing, management in their latest earnings call said that a part of recent revenue growth is partly the result of inflation-driven pricing. Inflation may not go away anytime soon, so this could drive short-term revenue growth as well. Furthermore, another long-term profit growth driver is the switch from temporary workers to full-time workers, which is expected to increase productivity. Lastly, the recent acquisition of Core-Mark, the largest and most-valued marketer of fresh and broad-line supply solutions to the convenience retail industry, should significantly drive both revenue growth and economies of scale.

For these reasons, I expect the 1-2 year growth to be significantly higher than the stated 3.7% expected industry growth.

Growth estimates by analysts in percentage:

|

Stock |

Revenue 2022 |

Revenue 2023 |

Earnings 2022 |

Earnings 2023 |

|

Performance Food |

66.6 |

11.1 |

88.1 |

26.0 |

|

Sysco |

28.4 |

7.3 |

113.9 |

36.0 |

Source: Analyst estimates from Seeking Alpha

Analysts expect both Performance Food and Sysco to achieve high growth rates compared to the expected industry growth rate. I suspect that this has to do with the short-term recovery of the business segment and acquisition revenue.

Margin analysis

I computed a key margins table. The first number in the cells in the following table refers to Performance Food, while the number between the parentheses refers to Sysco.

Accounting item as % of revenue: Performance Food(Sysco):

|

Accounting Item |

Last 4 Quarters |

2021 |

2020 |

2019 |

2018 |

|

Gross Profit |

10.87 (18.0) |

11.6 (18.2) |

11.44 (18.7) |

12.73 (19.0) |

13.01 (18.9) |

|

Operating Expense |

10.34 (14.8) |

10.94 (15.4) |

11.83 (17.3) |

11.29 (15.1) |

11.57 (14.9) |

|

Normalized EBITDA |

1.51 (4.6) |

1.8 (4.5) |

0.68 (3.0) |

2.22 (5.2) |

2.18 (5.3) |

|

Free Cash Flow |

0.17 (1.4) |

-0.41 (2.8) |

1.86 (1.7) |

0.9 (2.9) |

1.29 (2.5) |

|

Normalized Income |

0.09 (1.3) |

0.13 (1.0) |

-0.45 (0.4) |

0.84 (2.8) |

1.13 (2.4) |

Source: Seeking Alpha income statement

Distribution businesses often have relatively low margins. However, Performance Food has roughly half the margin that Sysco has, which could indicate a difference in pricing power. Nonetheless, future drivers for an increase in profit margins for Performance Food are the initiative towards more full-time workers, the further integration of its acquisition Core-Mark, further recovery of the business segment, and further economies of scale.

Valuation

I have calculated several valuation ratios to determine the market’s view of the companies.

Key valuation measures:

|

Stock |

Enterprise value/Revenue |

Enterprise value/EBITDA |

Enterprise value/Gross Profit |

Forward PS |

Forward PE |

|

Performance Food |

0.32 |

20.91 |

2.94 |

0.14 |

15.58 |

|

Sysco |

0.89 |

19.33 |

4.96 |

0.61 |

20.39 |

Source: Seeking Alpha

Let me, first of all, say that for both the companies the forward P/E is relatively low, which isn’t too crazy of a thought as these aren’t long-term high-growth businesses. Also, for Performance Food, you’ve got all of these drivers margin expansion for the short and medium-term, which I expect to result in a fairly low P/E ratio forwarded 2 to 3 years. Besides, in the current unstable market with inflation worries, Performance Food has shown to price in inflation quite well. With the business having a large footprint in the USA, being diversified, and operating in a stable industry, I believe that it’s a nice business to have in unstable times. To buy a stock like that for 15.58, with the growth opportunities in mind, I believe that Performance Food currently is a buy.

[ad_2]

Source link